As the crypto industry moves into its regulatory era, DeFi (Decentralized Finance) has become one of the top areas of focus for regulators worldwide. In recent years, DeFi has grown rapidly thanks to its permissionless, open, and transparent nature, along with automated on-chain execution, spawning a wide range of innovations: lending, trading, derivatives, stablecoins, and asset management. Unlike traditional financial institutions and centralized exchanges, DeFi protocols often lack a clearly identifiable operator, which makes applying existing regulatory frameworks a major challenge.

As the world's first crypto-asset regulatory framework to cover an entire regional market, MiCA's introduction marks the EU's establishment of a unified set of digital asset rules. However, compared to exchanges, stablecoin issuers, and custodians, DeFi occupies a more nuanced position under MiCA.

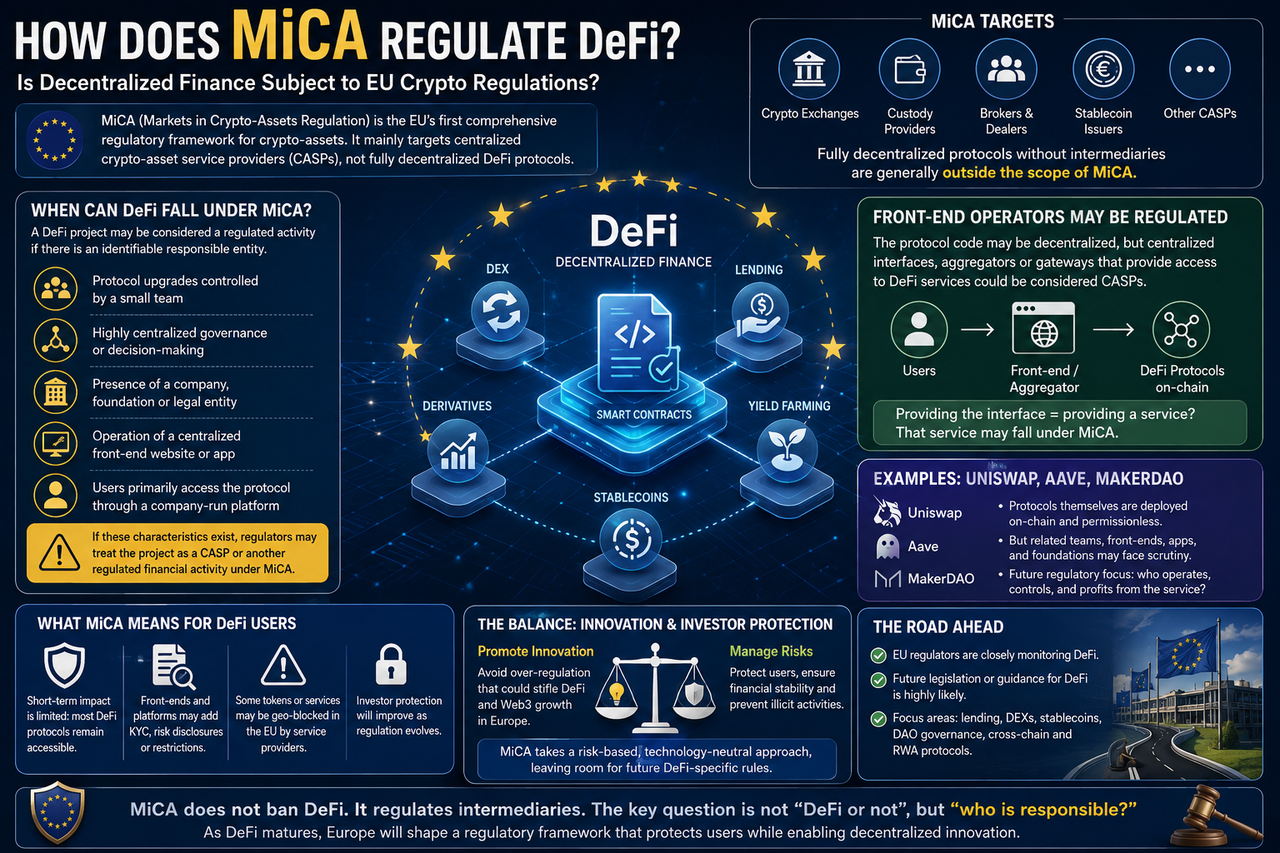

Does MiCA Directly Regulate DeFi?

Under current rules, MiCA does not establish a regulatory framework for fully decentralized protocols.

During MiCA's legislative process, the EU explicitly stated that services that are fully decentralized and involve no intermediary are, in principle, outside MiCA's scope.

This is because MiCA is built around the CASP (Crypto-Asset Service Provider) framework, targeting crypto exchanges, custodians, brokers, and other centralized entities that offer digital asset services.

If a DeFi protocol is truly autonomous—with no operating company, management team, or controlling party—then under the current MiCA text, it would generally not be considered a CASP and would not need a MiCA license.

That's why many in the industry believe DeFi is temporarily outside the reach of MiCA.

When Could DeFi Be Affected by MiCA?

While fully decentralized protocols may not be directly targeted, reality is often messier than theory. Many so-called DeFi projects still have development teams, operating companies, or foundations handling protocol upgrades, product maintenance, and marketing. In these cases, regulators may see an identifiable party to hold accountable.

Situations that could draw regulatory attention include:

- Protocol upgrades controlled by a small group

- Highly concentrated governance voting power

- A commercial entity responsible for daily operations

- A centralized front-end website for the project

- Users primarily accessing the protocol through a company-run platform

If these features are prominent, regulators may decide the activity is effectively a regulated financial service rather than a genuinely decentralized protocol. So whether a DeFi project is regulated depends not on its label, but on its actual operating model.

This is one of the most actively debated regulatory questions in Europe right now.

While many DeFi protocols are deployed on-chain, most users interact with them through official websites or apps. From a regulatory standpoint, smart contracts themselves may be hard to regulate, but the platforms that provide access could be subject to oversight.

For instance, if a company runs an aggregator platform that helps users access multiple DeFi protocols, regulators could consider it a digital asset service provider. In the future, EU regulatory focus is likely to shift from the protocol itself to user entry points and service providers.

How Does MiCA View DAO Governance?

DAOs (Decentralized Autonomous Organizations) are a core part of the DeFi ecosystem.

Theoretically, DAOs govern protocols collectively through token holders, without relying on traditional corporate structures, making them a key symbol of decentralization.

But in reality, many DAOs still suffer from governance concentration. For example, a few institutions may hold a large share of governance tokens, or the core development team may hold actual decision-making power. In such cases, regulators may reassess whether the DAO is truly decentralized.

Going forward, EU regulators are likely to focus on:

| Regulatory Concern |

Core Question |

| Governance token distribution |

Do a few entities control voting power? |

| Protocol upgrade authority |

Is it held by the core team? |

| Treasury management |

Is there a real controlling entity? |

| Legal liability |

Who bears responsibility for user losses? |

| Revenue distribution |

Does it resemble traditional financial products? |

So a DAO label does not automatically grant immunity from regulation.

Will MiCA Affect Uniswap and Aave?

For now, MiCA won't force Uniswap or Aave to apply for a CASP license.

However, if EU regulators later determine that a protocol has a controlling party or centralized operating team, the related business may face further scrutiny. For example:

| Protocol Type |

Likelihood of MiCA Regulation |

| Fully on-chain protocol |

Low |

| Protocol with a development team maintaining it |

Medium |

| Protocol operated by a commercial company |

High |

| Protocol offering custodial services |

High |

| Protocol providing fiat on-ramp services |

High |

So the regulatory focus will likely be on whether the operating model aligns with true decentralization, not just the protocol's name.

How Will MiCA Affect DeFi Users?

For everyday users, the short-term impact is limited. You'll still be able to access most DeFi protocols for lending, trading, staking, and more. But as regulatory frameworks evolve, you may notice gradual changes:

| User Experience |

Possible Changes |

| Wallet usage |

Largely unchanged |

| On-chain trading |

Largely unchanged |

| DeFi access points |

May add compliance requirements |

| Fiat on/off ramps |

Tighter scrutiny |

| KYC checks |

Some services may introduce them |

| Risk disclosures |

More information provided |

Overall, regulation is more likely to affect DeFi service providers than to directly limit on-chain protocol usage.

Will the EU Introduce Specific DeFi Regulations?

Industry consensus says yes.

While MiCA establishes a crypto asset regulatory framework, legislators acknowledged during its drafting that DeFi issues were not fully resolved.

The European Commission has repeatedly stated it will continue monitoring DeFi market developments and assess whether dedicated rules are needed.

Future focus areas may include: DeFi lending platforms, on-chain derivatives protocols, decentralized stablecoins, DAO governance systems, cross-chain financial protocols, and RWA on-chain financial products.

Balancing DeFi and MiCA Regulation

Regulators face the biggest challenge of balancing innovation and risk.

Too strict, and they may stifle Europe's Web3 innovation and capital flow; too lenient, and they risk inadequate investor protection and systemic risk.

MiCA's current approach is to prioritize regulating centralized service providers while observing how the DeFi market evolves. This incremental regulatory strategy helps avoid prematurely stifling innovation and builds experience for crafting more precise DeFi rules later.

In that sense, MiCA is not the end of DeFi regulation, but rather the beginning of Europe's digital asset regulatory journey.

Summary

MiCA is the EU's first unified crypto regulatory framework, but its main targets are centralized entities like exchanges, custodians, and stablecoin issuers—not fully decentralized DeFi protocols. Under current rules, truly operator-less, controller-less DeFi projects generally aren't subject to MiCA.

In practice, however, most DeFi projects still have development teams, governance organizations, or operational platforms, so parts of their business may attract regulatory attention. As the DeFi market grows, the EU is likely to introduce specific rules for decentralized finance.

FAQs

Do fully decentralized protocols need a MiCA license?

In principle, no. If a protocol has no operating entity, management team, or intermediary, it generally falls outside CASP regulation.

Are DAOs regulated by MiCA?

DAOs aren't automatically regulated. But if governance is highly concentrated or a controlling team exists, regulators may reassess their legal status.

Are Uniswap and Aave subject to MiCA?

For now, they won't be forced to apply for a CASP license, but their operating teams or service entry points could face regulatory scrutiny in the future.

Will MiCA affect DeFi users?

Short-term impact is limited. Users can still access most DeFi protocols. However, some entry platforms may add KYC, risk disclosures, and other compliance measures.