On July 1, 2026, Beijing time, Credo Technology Group Holding (NASDAQ: CRDO) shares surged 10.69%, closing at $271.95. During the session, the stock rallied from a low of $244.06 to a high of $275.43, with a range of 12.77%. Trading volume reached 8.0721 million shares, and total market capitalization rose to $50.713 billion.

CRDO's move was not an isolated event. In June 2026, optical communication and high-speed interconnect-related concept stocks repeatedly became market focuses. Elon Musk's entity acquired optical communication startup Mesh Optical Technologies, and the FTC has cleared the antitrust review. NVIDIA CEO Jensen Huang explicitly stated at Computex 2026 that connectivity has become a "necessity" for AI infrastructure. Marvell CEO Matt Murphy went further, asserting that the true bottleneck in AI infrastructure is no longer computing power or memory, but connectivity.

Market signals and industry judgments are pointing in the same direction: the competition in AI data centers is shifting from an "arms race in computing power" to a "race in network efficiency."

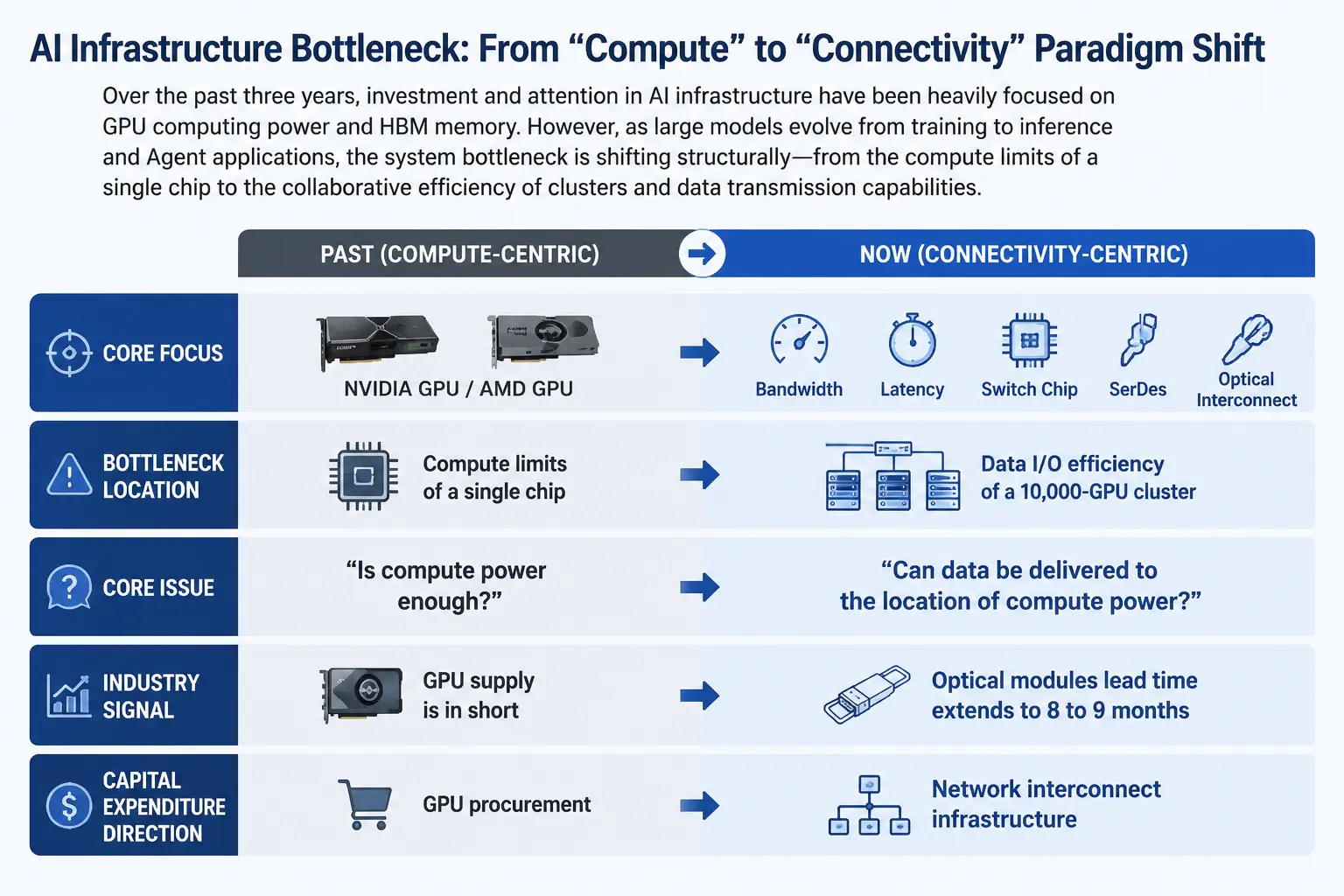

From Computing Power to Connectivity: A Paradigm Shift in AI Infrastructure Bottlenecks

Over the past three years, the narrative of global AI infrastructure investment has been highly concentrated — GPU procurement and HBM memory stacking formed the consensus that "computing power is the moat." NVIDIA's GPUs are in short supply, AMD's catch-up, and the capital expenditure race among major cloud providers were the absolute main themes of market attention.

But this narrative is undergoing a structural change. As large models move from the training phase to the inference and agent application phase, the form of AI workloads has fundamentally changed. The training phase is characterized by compute intensity but relatively regular communication patterns; the inference and agent phases involve real-time data exchange among a massive number of distributed compute nodes. Data flow has surged, and the demands on bandwidth and latency far exceed what single-point compute improvements can cover.

System bottlenecks are shifting from the compute limit of a single GPU to the collaboration efficiency of clusters of tens of thousands or even millions of GPUs. Industry test reports from H3C show that data I/O bottlenecks in a 10,000-GPU cluster can cause GPU idle waiting time to account for over 40% — meaning expensive compute chips spend nearly half their time waiting for data movement.

This is not a lack of computing power, but that data cannot reach where the computing power resides. In June 2026, Google was reportedly unable to provide Meta with the full compute capacity required for its AI model "Gemini." Multiple media reports pointed out that the shortage of AI infrastructure has moved from theoretical speculation to real-world constraints, and even the world's largest tech companies cannot obtain unlimited computing resources. The market significance of this event is: when even a leading player like Google faces supply constraints, the bottleneck issue has shifted from "whether it will happen" to "how severe it is."

AI infrastructure bottleneck migration path diagram

Physical Bottlenecks in the Supply Chain: Optical Module Lead Times Extended to 8–9 Months

If changes in market narrative represent a cognitive shift, then data at the supply chain level provides more solid validation.

According to supply chain information, the shortage of key components for AI data center construction is worsening. Intel server CPU lead times have extended from around 12 weeks to about 26 weeks, while AMD CPU lead times have reached 16 weeks. But the most severe bottleneck is not CPUs, but high-speed optical modules related to the InfiniBand architecture — lead times have stretched to 8 to 9 months, even exceeding CPU lead times.

The root cause of tight optical module supply is the shortage of upstream optical communication chips. Indium phosphide (InP)-related optical communication chips and laser components face multiple constraints such as high technical barriers and difficulty in expanding production capacity. Some supply chain analysts believe that due to demand far exceeding supply, this shortage will continue for several years.

This supply chain bottleneck reveals a key fact: the expansion speed of AI data centers is being limited by the supply capacity of network interconnection components. Even if GPU supply is sufficient, data centers cannot be put into production as planned if optical modules and high-speed interconnect components cannot be delivered.

High-Speed Interconnect Technology Stack: SerDes, Switch Chips, and Optical Interconnect

Understanding why "network interconnect" has become a bottleneck requires understanding the data flow path within AI data centers.

Communication in AI clusters can be divided into several layers: chip-to-chip interconnect within a rack (scale-up), switch interconnect between racks (scale-across), and long-distance transmission between data centers (scale-out). Each layer involves different technologies and components.

SerDes (Serializer/Deserializer) is the most fundamental and basic technology layer. Its function is to convert parallel data into serial data for high-speed transmission and then restore it at the receiving end. As data center bandwidth demands continue to rise, SerDes rates are evolving from 56G to 112G and even 224G. The global SerDes market is expected to grow from $1.2 billion in 2025 to $1.33 billion in 2026, a CAGR of about 10.8%. Although the absolute scale is not large, SerDes is the foundation layer of almost all high-speed interconnect solutions — without SerDes, there is no high-speed data communication.

Switch chips are the core of network topology. Crehan Research predicts that total sales of Ethernet switches will exceed $250 billion over the next five years, mainly driven by AI-driven data center bandwidth demand growth. More notably, Crehan predicts data center bandwidth will grow 15-fold over the next five years. This magnitude of growth means existing network infrastructure will face unprecedented pressure.

Optical interconnect is seen as the ultimate solution to break through the physical limits of copper cables. The laws of physics dictate the "copper wall": doubling bandwidth halves the effective transmission distance of copper cables. When evolving to 1.6T and above, copper's survival space within the rack is extremely compressed, and optical interconnect is penetrating from the backbone network into the rack. NVIDIA's Jensen Huang put it this way: use copper as long as possible, use optics where necessary.

2026 is considered by the industry as the watershed year for AI data center optical interconnect transitioning from introduction to mass production. The real volume increase is not in CPO switches for scale-out, but in the GPU scale-up domain. This means optical interconnect is moving from connections between data centers deep into the server rack, directly connecting GPU to GPU.

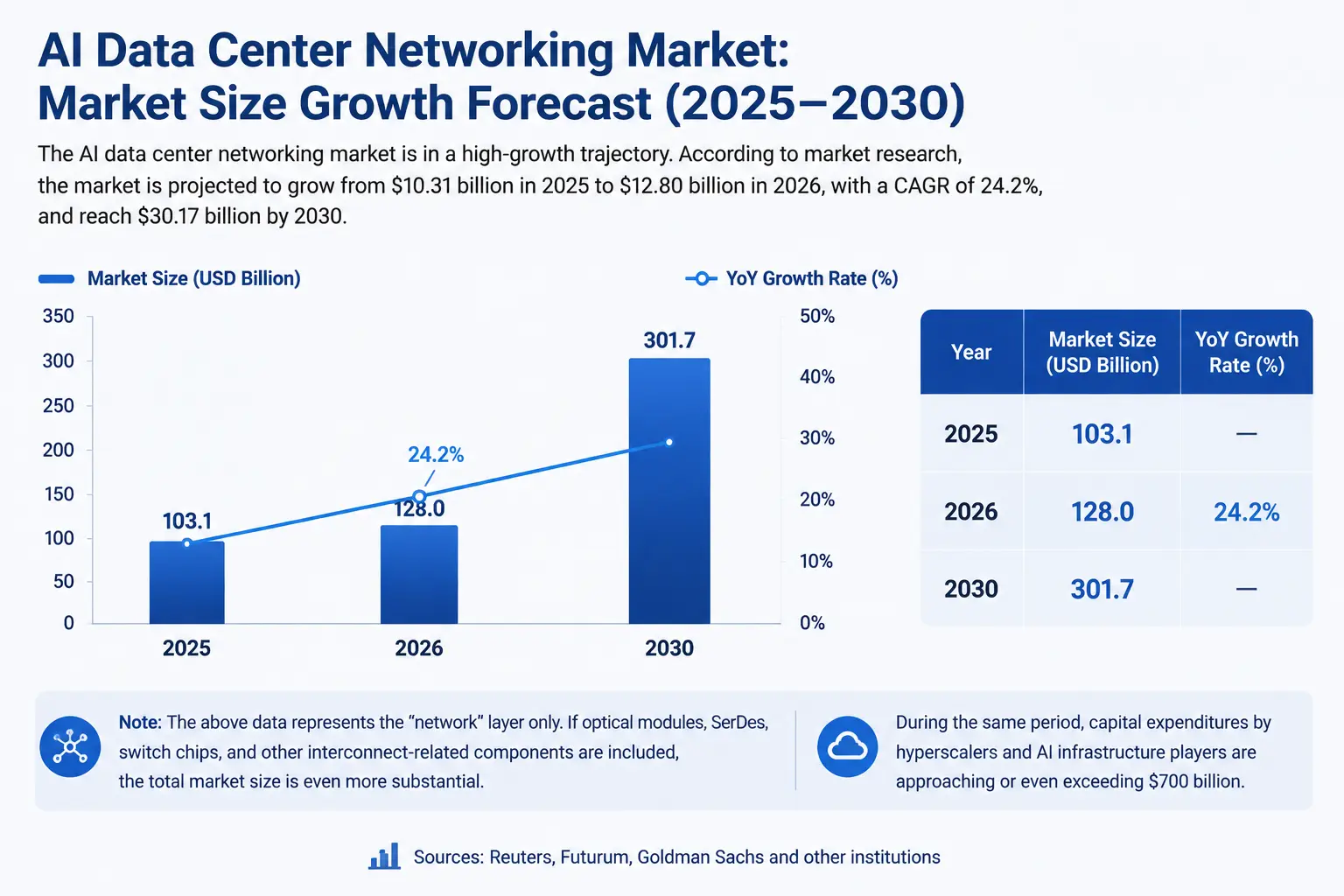

Quantifying the Market Space: A Hundred-Billion-Dollar Track Taking Shape

The market space for AI data center network interconnect is rapidly becoming visible.

According to market research data, the AI data center network market is expected to grow from $10.31 billion in 2025 to $12.8 billion in 2026, a CAGR of 24.2%. By 2030, this market is expected to reach $30.17 billion.

This is only the "network" level statistics. Including all interconnect-related components such as optical modules, SerDes, and switch chips, the overall market size will be even larger.

At the capital expenditure level, according to estimates from Reuters, Futurum, and Goldman Sachs, by 2026, the capital expenditure of major cloud vendors and AI infrastructure-related players will approach or even exceed $700 billion. Within this magnitude of capex, network interconnect is becoming a key cost item alongside GPUs.

CRDO's financial data provides micro-level validation. In the fourth quarter of fiscal 2026, Credo's revenue reached $437 million, up 157% year-over-year and 7.4% quarter-over-quarter. Full-year revenue exceeded $1.3 billion, more than tripling from the previous year; non-GAAP net profit grew more than fivefold to $662 million. The company's revenue guidance for the first quarter of fiscal 2027 is $465 million to $475 million.

These data collectively point to one conclusion: high-speed interconnect is not a "concept" but an incremental market being validated with real money.

AI data center network interconnect market size growth chart

Competitive Landscape: Who Is Laying Out the "Data Highway"

Participants in the high-speed interconnect track are rapidly expanding, and the competitive landscape is becoming clearer.

Credo Technology (CRDO) focuses on high-speed connectivity solutions, covering SerDes, active electrical cables (AEC), and optical DSPs, directly serving the high-speed interconnect needs of AI data centers. BNP Paribas gives it a target price of $275. On July 1, CRDO's stock surged 10.69% to $271.95, very close to this target.

Marvell — its CEO personally stated at Computex 2026 that "connectivity is the bottleneck," and its optical communication DSP and interconnect product lines are benefiting from this trend.

Broadcom, as a core supplier of switch chips and SerDes, occupies an important position in the AI data center network field.

Optical module and communication manufacturers include Coherent, Lumentum, and Zhongji Innolight, directly benefiting from the explosion of optical interconnect demand.

Cloud vendor self-development is another thread that cannot be ignored. Major cloud vendors such as Google, AWS, and Microsoft are all developing their own network chips and interconnect solutions to reduce dependence on third-party suppliers and optimize cluster performance.

Notably, Elon Musk entered the optical communication field by acquiring Mesh Optical Technologies. Mesh's core product, Alpha C1, supports 1.6T and 800G rates with only one-third the power consumption of similar modules. The signal of this acquisition is that even companies like SpaceX and xAI, which are labeled as "compute-centric," now see "connectivity" as a strategic asset that must be controlled independently.

Risks and Constraints: Structural Issues Behind the Boom

The growth logic of the high-speed interconnect track is clear, but not without constraints.

Supply chain concentration risk is the primary issue. Core raw materials for optical modules, such as indium phosphide (InP)-related chips and laser components, face supply shortages, high technical barriers, and long capacity expansion cycles. This upstream bottleneck may in turn limit the capacity expansion of interconnect components themselves, creating a "bottleneck of bottlenecks."

Uncertainty in technology roadmaps cannot be ignored. Optical vs. copper interconnect, pluggable optical modules vs. CPO (co-packaged optics), and different vendors' interconnect protocol standards — these technology roadmap battles are still ongoing. When the industry evolves to 1.6T and above, technologies like CPO are seen as key to breaking density and power bottlenecks, but their mass production capability and cost structure have not been fully validated.

Valuation vs. expectation divergence has already appeared in some targets. Based on the closing price of $271.95 on July 1, CRDO's static P/E ratio is approximately 108.39 times, meaning the market has already given full, even aggressive, pricing to its future growth. Any below-expectation financial performance or industry growth slowdown could trigger valuation restructuring.

Geopolitical factors also pose potential risks. The optical communication industry chain involves high-end chip manufacturing, advanced packaging, and other segments. Geopolitical frictions could affect supply chain stability and cost structures.

Summary

Competition in AI data centers is entering a new phase. Over the past two years, the market's focus was "who has more GPUs"; in the next two years, the market may focus more on "who can make GPUs work more fully."

When GPUs in a 10,000-GPU cluster spend 40% of their time waiting for data, when optical module lead times stretch to 9 months, when the world's largest tech companies cannot obtain sufficient compute capacity — these signals collectively point to a clear industry trend: the bottleneck in AI infrastructure is shifting from "computing power production" to "computing power connectivity."

High-speed interconnect, bandwidth, latency, SerDes, optical modules — these areas once considered "infrastructure for infrastructure" are moving from behind the scenes to the forefront. CRDO's 10.69% gain on July 1, with an intraday high of $275.43, sent a clear signal to the market: capital is repricing the value of interconnect.

For investors, understanding the migration path of bottlenecks in the AI industry chain may be more forward-looking than simply tracking GPU shipments. Computing power is the engine of AI, but connectivity is the blood vessel — without blood vessels, no matter how powerful the engine, it cannot drive the entire system.

FAQ

Q1: What are the core drivers of the AI data center interconnect bottleneck?

As large models move from training to inference and agent applications, data flow surges, and demands on bandwidth and latency far exceed what single-point compute improvements can cover. The system bottleneck shifts from single-GPU computing power to the collaboration efficiency of clusters of tens of thousands or even millions of GPUs, essentially a network connectivity issue.

Q2: What role does SerDes play in AI data center interconnect?

SerDes (Serializer/Deserializer) is the foundational layer technology for high-speed data transmission. It converts parallel data into serial data for high-speed transmission and restores it at the receiving end. It is the basis of all high-speed interconnect solutions. As data center bandwidth demands evolve to 112G and even 224G, the importance of SerDes continues to rise.

Q3: Why have optical modules become a major bottleneck in AI data center expansion?

Lead times for InfiniBand architecture-related optical modules have extended to 8 to 9 months, exceeding CPU lead times of 6 to 9 months. The core reason is that upstream indium phosphide (InP) optical communication chips and laser components face multiple constraints such as high technical barriers and difficulty in expanding production capacity, and the supply shortage is expected to last for several years.

Q4: What is the market size for AI data center network interconnect?

The AI data center network market is expected to grow from $10.31 billion in 2025 to $12.8 billion in 2026, a CAGR of 24.2%, and is expected to reach $30.17 billion by 2030. By 2026, the capital expenditure of major cloud vendors and AI infrastructure players is approaching or exceeding $700 billion.

Q5: What risks should investors watch in the high-speed interconnect track?

Investors should watch supply chain concentration risks (shortage of raw materials like indium phosphide), technology roadmap uncertainty (optical vs. copper interconnect, CPO mass production progress), the already full or aggressive pricing of some targets (CRDO's static P/E ratio is about 108 times), and the potential impact of geopolitics on the high-end optical communication chip supply chain.