On June 25, 2026, Bitcoin's price fell below the $60,000 mark. According to Gate market data, Bitcoin touched a daily low of $59,023, the lowest level since October 2024. This price level is down more than 50% from its all-time high above $126,000 in October 2025.

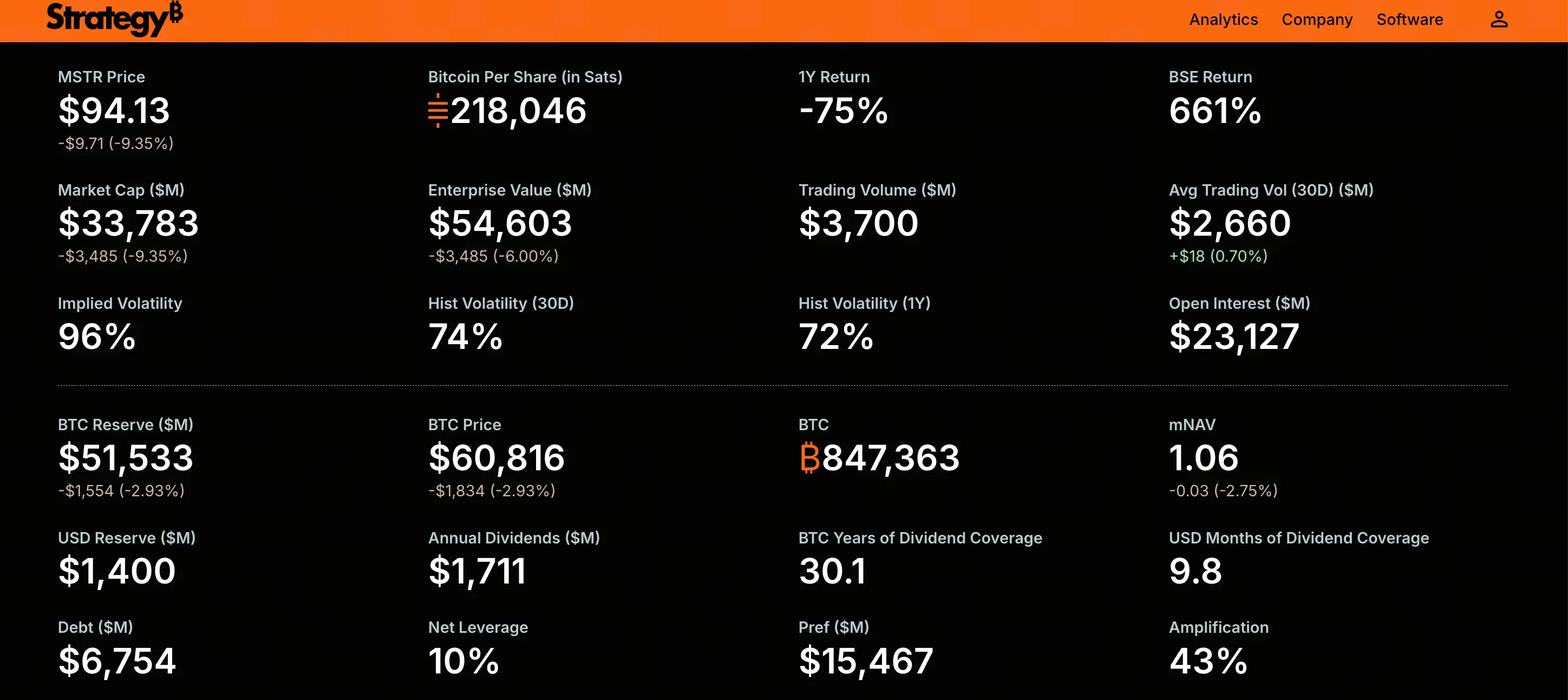

The continued decline in Bitcoin directly transmitted to its largest corporate holder. Strategy (formerly MicroStrategy) common stock MSTR fell below $100 during intraday trading on June 25, hitting a low of $92.5, the first time below that threshold since March 2024. MSTR fell about 9.2% on the day, after a cumulative decline of about 20% over the previous five trading days.

Meanwhile, Strategy's flagship preferred stock STRC also faced significant selling pressure. As of June 25, STRC was trading around $80.7, down over 18% in the past month.

The simultaneous weakening of MSTR and STRC indicates that the focus of market concern is no longer limited to Bitcoin's own volatility, but directly on whether Strategy can sustain its business model that relies on preferred stock dividends and continuous financing.

Why the Preferred Stock STRC Is Pegged at $100 and Continues to Trade Below Par

STRC is a variable-rate perpetual preferred stock issued by Strategy, designed to trade around $100 par value, providing investors with variable dividends backed by the company's Bitcoin reserves. The core logic of the product is built on price stability — as long as STRC remains near par value, the company can continuously raise funds through automatic issuance mechanisms to accumulate Bitcoin.

However, STRC has not traded at par value since mid-April 2025. This fall below $100 and continued decline reflects a combination of multiple factors.

The decline in Bitcoin's price is a direct trigger. STRC's entire value proposition depends on the quality of Strategy's Bitcoin reserves. When Bitcoin fell about 40% from its all-time high, investor confidence in the instrument was directly impacted.

Forced liquidation of leveraged positions exacerbated the downward momentum. Many investors entered STRC with leverage, expecting the $100 anchor price to hold. When the price began to decline, margin calls triggered automatic selling, creating a vicious cycle of price decline and forced liquidation.

Market concerns over dividend sustainability are heating up. Investors are beginning to question whether the company has sufficient cash flow to cover the rigid dividend payment obligations of the preferred stock.

Benchmark Equity Research analysts point out that STRC's decline is not a product malfunction but the structure operating as designed — when the actual dividend yield is lower than the market-required yield, the price naturally moves down to push up the actual yield. Based on the current trading price of around $84-$87, with an 11.5% coupon on $100 par value, the actual market yield for new buyers has risen to about 13%-14%. This means investors are demanding higher risk compensation.

How Preferred Stock Dividend Obligations Create Rigid Cash Pressure

Dividends on STRC and other preferred stock series are rigid cash obligations that cannot be paid directly with the book value of Bitcoin. This structural feature constitutes a continuous cash drain in the current market environment.

Strategy's annual preferred stock dividend commitments have surged from about $300 million at the beginning of 2026 to about $1.2 billion. Estimates vary by source; some analysts indicate the annual dividend obligation could be close to $1.7 billion. Whichever figure is used, this number represents significant pressure relative to the company's cash reserves.

As of June 2026, Strategy's cash reserves are about $1.4 billion. Based on an annual dividend obligation of $1.2 billion, existing cash reserves can only cover about 14 months of dividend payments. Data from CryptoQuant shows that dividend coverage has plummeted from over seven years to about 14 months.

More notably, Strategy recently repurchased $1.5 billion of convertible senior notes due in 2029, further reducing cash available to support dividend payments. Under the dual pressure of a narrowing financing window and declining cash reserves, the company's ability to maintain preferred stock dividends is facing increasingly stringent scrutiny.

What the Inversion of MSTR's Market Cap and Bitcoin Holdings Means

As of June 24, 2026, Strategy holds 847,363 Bitcoins, accounting for about 4% of the total supply. The total purchase cost is about $64.1 billion, with an average purchase price of about $75,650 per coin. At a Bitcoin price of $60,000, the market value of the holdings is about $50.8 billion, with an unrealized loss of about $11 billion to $13 billion.

Meanwhile, MSTR's market cap has fallen below the fair value of its Bitcoin holdings. Based on about 351.6 million shares outstanding and a stock price near $100, MSTR's market cap is about $35 billion. This means the market is not only giving no premium to Strategy's valuation beyond its Bitcoin holdings, but is actually trading at a price below the liquidation value of its Bitcoin assets.

This discounted state has profound signal significance. For most of 2023 to 2024, MSTR generally traded at a premium to its Bitcoin holdings value. The premium reflected market confidence in Strategy's ability to continuously accumulate Bitcoin — investors were willing to pay extra for 'leveraged Bitcoin exposure.' Now the premium has turned into a discount, meaning the market no longer believes the company can continue to expand its Bitcoin reserves on favorable terms.

Why the Financing Cycle Stalls After MNAV Falls Below the Critical Threshold

The core driving indicator of Strategy's business model is MNAV (Market Net Asset Value) — the ratio of the company's market cap to the net value of its Bitcoin holdings. This indicator determines whether the company can accumulate Bitcoin through stock issuance without diluting existing shareholders.

When MNAV is above a certain threshold (widely considered around 1.2x), the company can raise funds by issuing new shares to buy Bitcoin, thereby increasing the Bitcoin content per share. This is a positive reinforcement cycle: premium financing → buy Bitcoin → Bitcoin appreciates → premium expands → more financing capacity.

However, when MNAV falls below 1x, this cycle reverses. According to Jason Huang, founder of NextGen Venture, Strategy's recent ATM stock issuances have diluted its MNAV multiple to about 1.1x. With MSTR falling below $100, MNAV has further slipped below 1x.

MNAV below 1x means that buying Bitcoin through stock issuance would directly dilute the Bitcoin content per share, which is unfavorable to existing shareholders. This effectively closes the company's core equity financing channel. Meanwhile, STRC trading below par value also blocks the preferred stock financing channel.

With both financing paths blocked simultaneously, Strategy faces a fundamental question: if it cannot raise new capital on favorable terms, how will it meet its growing preferred stock dividend obligations?

From 'Only Buy, Never Sell' to the First Sale: Market Implications of the Narrative Shift

From late May to early June 2026, Strategy sold 32 Bitcoins, cashing out about $2.5 million, to pay dividends for STRC. This is the first time the company has sold Bitcoin since 2022.

In terms of quantity, 32 Bitcoins are negligible relative to the total holdings of 847,363. But symbolically, this move broke the 'only buy, never sell' narrative that Strategy has adhered to for years. Michael Saylor had repeatedly conveyed to the market the commitment to never sell Bitcoin, and this small-scale sale — for whatever reason — shook the foundation of that narrative.

The market reacted swiftly. The accelerated decline of STRC partly reflects investors pricing in the possibility that 'the company may be forced to sell more Bitcoin.' Once the market forms an expectation that Strategy may tap its Bitcoin reserves to pay dividends, its valuation logic will undergo a fundamental shift — it is no longer just a leveraged Bitcoin proxy asset, but has become a financial engineering company that needs to balance holdings, dividends, and financing costs with difficulty.

The potential impact of this narrative shift is not limited to Strategy itself. As the world's largest institutional Bitcoin holder, if Strategy is perceived as a 'potential net seller,' this could have a psychological impact on the supply-demand dynamics of the Bitcoin market.

Possible Evolution Paths Under Sustained Pressure

The core contradiction of the current situation facing Strategy can be summarized as: a widening gap between narrowing financing channels and expanding cash obligations.

From a balance sheet structure perspective, the company holds over 847,000 Bitcoins and has about $8 billion in debt, which is unsecured low-interest debt with no margin call mechanism. In the most extreme case, the company could gradually sell Bitcoin to cover dividends; this path is technically feasible.

But 'feasible' and 'costless' are two different things. Large-scale Bitcoin sales could trigger price shocks and disrupt market sentiment. More importantly, once the company is perceived by the market as being in a 'sell coins to maintain operations' state, its core investment narrative will be irreversibly weakened.

Another evolution path is for Bitcoin's price to recover above the company's average cost. If Bitcoin returns above $75,000, MNAV could re-expand and the financing cycle might restart. But this essentially depends on the external market environment, not factors the company can control.

The most concerning scenario may not be a sharp drop in Bitcoin, but Bitcoin consolidating at low levels for a long time. In an environment lacking upward momentum, continuous dividend cash consumption will slowly erode the company's financial buffer, and the blockage of financing channels will worsen the problem over time.

Frequently Asked Questions (FAQ)

Q: Is the 'anchor price' of $100 for STRC guaranteed?

A: No. STRC is designed to trade around $100, but the company does not promise or guarantee that price. When the market-required yield is higher than the product's coupon, the price naturally moves down to increase the actual yield. The current discount reflects investors' demand for higher risk compensation.

Q: What impact does MSTR falling below $100 have on Bitcoin's price?

A: The decline of MSTR itself does not directly determine Bitcoin's price, but the chain reaction it triggers may have an indirect impact. If Strategy is forced to sell a large amount of its Bitcoin reserves due to cash pressure, it could cause additional selling pressure on the Bitcoin market. Currently, the company has only made a small sale of 32 Bitcoins, but the market has already reacted.

Q: Will Strategy be forced to liquidate its Bitcoin holdings?

A: There is currently no forced liquidation mechanism. The company's debt is unsecured, with no margin call clauses, and the earliest maturity is 2028. The company can choose to gradually sell Bitcoin to cover dividends, but this comes at a narrative cost. The current pressure is more reflected in the structural contradiction of limited financing capacity and accelerated cash consumption.

Q: What is the current actual yield of STRC?

A: The coupon dividend rate of STRC is 11.5%. However, because the trading price is far below the $100 par value (around $84-$87), the actual market yield for new buyers has risen to about 13%-14%. This yield increase is compensation for the additional risk investors are taking.

Q: What is MNAV and why is it important?

A: MNAV (Market Net Asset Value) is the ratio of the company's market cap to the net value of its Bitcoin holdings. When MNAV is above 1.2x, the company can buy Bitcoin through stock issuance without diluting shareholders. When MNAV is below 1x, issuance directly dilutes the Bitcoin content per share, so the financing cycle stalls. Changes in MNAV directly determine whether Strategy's business model can continue to operate.