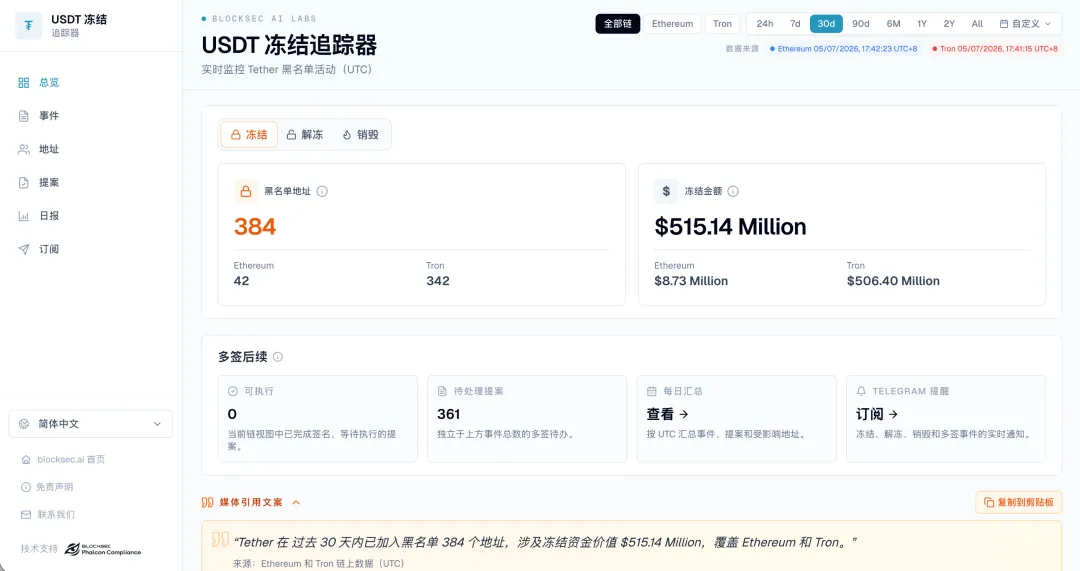

According to a May report from blockchain security firm BlockSec, titled “Stablecoin Issuer Freeze Risk and Treasury Security Management Whitepaper,” its USDT Freeze Tracker on-chain statistics show: as of May 7, over the past 30 days, Tether has added a total of 384 addresses to the blacklist across the Ethereum and Tron networks, involving frozen funds of about $515 million.

Freeze Trigger Mechanisms: The Whitepaper Summarizes Four Typical Scenarios

(Source: BlockSec)

According to BlockSec’s whitepaper, four typical trigger scenarios for issuers to execute freezes of USDT (Tether) and USDC (Circle) are as follows. The relevant basis comes from Tether, Circle, and OFAC’s official publicly released documents:

· Formal requests from law enforcement, judicial, and regulatory authorities

· Matching a sanctions list (such as OFAC) or the presence of sanctions-related risk

· High-risk fund flows such as scams, theft, money laundering, or terrorist financing

· Active or semi-active freeze measures triggered by technical migrations or changes in chain support

The whitepaper also cites an OFAC official statement noting that the publicly listed digital-asset addresses are usually not exhaustive, and risk identification needs to extend to related flows and multi-hop provenance.

Four Typical Governance Blind Spots in Corporate Treasury Security

According to BlockSec’s whitepaper, companies face four typical governance blind spots in stablecoin freeze-risk management:

On-chain risk of addresses and counterparties is not visible: companies usually lack visibility into their customers’ and counterparties’ on-chain addresses, clusters of related addresses, and historical interactions.

On-chain historical linkage across multiple hops is not visible: once “historical contamination” enters the main fund pool, the risk of a single incoming transaction may escalate into the fund pool’s overall availability risk.

Over-concentrated wallet and fund-pool design: when assets are consolidated into a single wallet and a single chain, a freeze affecting a single point can lead to a shutdown of the entire business.

Lack of continuous monitoring mechanisms: OFAC sanctions lists are continuously updated, and one-time screening cannot replace ongoing monitoring.

According to the whitepaper, BlockSec recommends that companies build incident attribution capabilities before risk occurs—clearly assessing which batch of assets may face risk, whether the risk originates from upstream activity or historical contamination, and whether it has spread to the main fund pool—so they have a basis for effective communication with issuers.

Stablecoin Market Scale: Third-Party Data

Based on DefiLlama data (May 2026), the global total market cap of stablecoins has surpassed $320 billion. According to an on-chain analytics dashboard jointly published by Visa and Allium (as of May 7, 2026), over the past 30 days, the global on-chain raw transaction volume of stablecoins reached $7.6 trillion; after excluding adjustments for internal transfers within institutions, the adjusted transaction volume was $1.2 trillion.

FAQ

What is the data source for BlockSec’s freeze figures in the whitepaper?

According to BlockSec’s whitepaper, the freeze statistics come from BlockSec’s proprietary USDT Freeze Tracker on-chain tool, covering Tether’s address blacklist records and unfreeze dynamics on the Ethereum and Tron networks, with statistics compiled up to May 7, 2026.

After stablecoins are frozen in a corporate treasury, can the assets be recovered?

According to BlockSec USDT Freeze Tracker data, over the past 30 days, Tether has unfrozen 88 addresses, corresponding to funds of about $22.29 million. BlockSec’s whitepaper states that freezing does not necessarily mean the assets are permanently unable to be restored; the key prerequisite is that the company can clarify the trigger reason promptly and communicate effectively with the issuer.

How does the issuer freeze-risk of stablecoins differ from traditional private-key security risk?

According to BlockSec’s whitepaper, traditional private-key security risk targets “who controls the address,” whereas issuer freeze risk means the address private keys remain controlled by the company, but the tokens themselves are restricted in circulation and usability due to the issuer’s control mechanisms at the contract level, redemption level, or chain support layer.