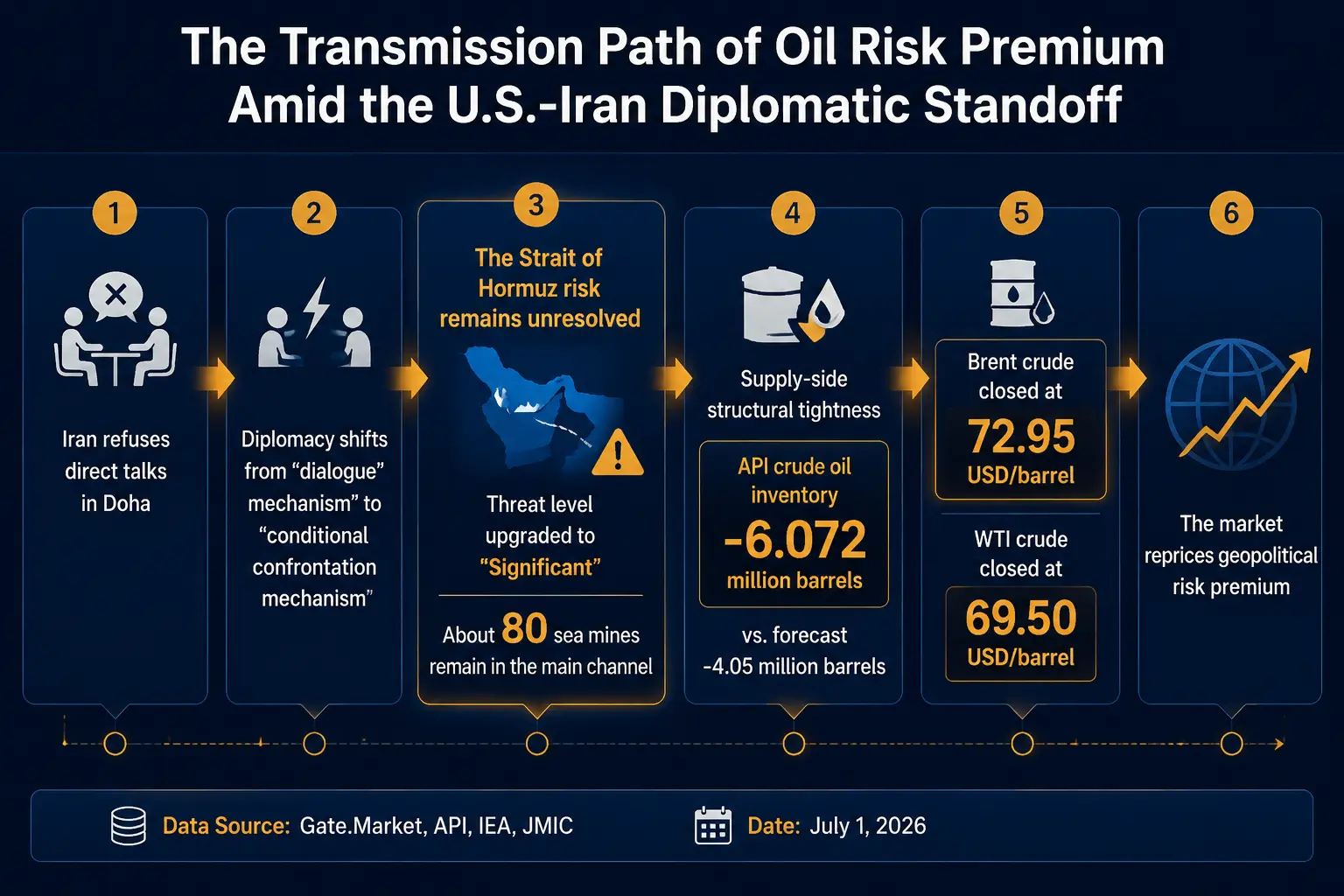

On July 1, 2026, the global asset market received a signal that was not entirely unexpected but nonetheless significant: Iran formally denied plans for a direct meeting with the United States in Doha. The previous day, U.S. President Trump posted on social media that Iran had proposed talks and that "talks will be held in Doha tomorrow." However, on June 30, Iranian Foreign Ministry Spokesperson Bagheri stated at a regular press conference that "no meetings at any level with the U.S. are scheduled for the coming days." Qatar also confirmed on the same day that there were no plans for a high-level U.S.-Iran meeting in Doha, though technical negotiations between the two sides were continuing in various forms.

This is not a simple change in diplomatic schedule. The shift from a "dialogue mechanism" to a "conditional confrontation mechanism" signals that the global market is moving from "negotiable geopolitical conflicts" into a "structural stalemate cycle" — where risk no longer depends solely on event escalation, but more on the persistent uncertainty triggered by the "failure of diplomacy itself."

Analysis from three perspectives: First, how does the U.S.-Iran diplomatic stalemate restructure the risk premium pricing logic of the crude oil market; Second, how do oil price fluctuations transmit to the crypto asset market through macro liquidity channels; Third, under this structural shift, the specific reactions and capital flow signals of Bitcoin, Ethereum, and stablecoin markets.

Iran Rejects Doha Meeting: Diplomacy Moves from "Dialogue" to "Conditional Confrontation"

The timeline of events itself constitutes an important market signal.

On June 29, Trump posted on social media claiming that Iran had requested talks and that "talks will be held in Doha tomorrow." On the same day, CNN reported, citing two U.S. officials, that U.S. Special Envoy Witkoff was en route to Doha. However, on June 29, Iran indicated that it would not hold any talks with the U.S. in the coming days. On June 30, Iranian Foreign Ministry Spokesperson Bagheri further clarified at a regular press conference, denying plans for any talks with the U.S. at any level in the near future.

What is noteworthy is not just the "rejection" itself, but the conditional logic behind the rejection. Bagheri stated that on July 1, Iran might discuss the implementation of a Memorandum of Understanding (MoU) with Qatar, including terms for unfreezing Iranian frozen assets. The timing of the start of final negotiations with the U.S. depends on the implementation of Articles 1, 5, 10, and 11 of the MoU. In other words, Iran has made the fulfillment of specific terms such as "asset unfreezing" a precondition for entering direct dialogue.

Meanwhile, after arriving in Doha, U.S. Special Envoy Witkoff and Trump's son-in-law Kushner only met with intermediaries such as Qatar's Prime Minister and Foreign Minister, and did not directly contact the Iranian delegation. A spokesperson for Qatar's Foreign Ministry said future contacts would be limited to the technical level. The U.S. side took a positive view of the discussions in Doha, but technical talks were ongoing.

The core characteristic of this landscape is: diplomacy has evolved from a "dialogue mechanism" where both sides sit together, to a "conditional confrontation mechanism" where you first meet my conditions before I consider talking. Analysts believe that while political will for dialogue between the U.S. and Iran still exists, mutual trust is insufficient, making it difficult to advance the political process. For the global market, this state of "low negotiation elasticity" means the time window for resolving conflicts is extended, transforming uncertainty from a "one-time event" into a "persistent condition."

Crude Oil Market: Risk Premium Repricing Underway

The transmission of the U.S.-Iran diplomatic stalemate to the crude oil market is direct and rapid, but intraday volatility is evident.

According to Gate data, as of July 1, 2026, Brent crude futures stood at $72.77 per barrel, down 1.45% over 24 hours, with an intraday range of $72.76–74.84; WTI crude futures stood at $69.33 per barrel, down 1.92% over 24 hours, with an intraday range of $69.31–71.64.

Cross-verified from multiple market data sources, benchmark spot/settlement prices: Brent crude closed at $72.95 per barrel, WTI crude at $69.50 per barrel. In early Asian trading, Brent briefly rose 0.45% to $73.28/barrel, WTI up 0.49% to $69.84/barrel; then pushed higher to Brent $73.45 (+0.69%) and WTI $70.13 (+0.91%). Notably, WTI crude futures posted their largest quarterly drop since early 2020 in the just-concluded second quarter.

Geopolitics → Crude Oil Risk Premium Transmission Path Diagram

This oil price reaction does not stem from a sudden change in supply-demand fundamentals, but from the market repricing geopolitical risk premium.

First-layer logic: The Strait of Hormuz risk remains unresolved. The Strait of Hormuz handles about 20% of global oil seaborne trade. Although shipping has gradually resumed after the conflict, the risk has not dissipated. The U.S.-led Joint Maritime Information Center (JMIC) has raised the maritime security threat level in the Strait of Hormuz from "medium" to "substantial," citing attacks on merchant vessels and the ongoing threat from mines and unexploded ordnance. The latest assessment from the International Maritime Organization (IMO) shows that approximately 80 mines remain in the traditional main channel of the strait, and it is expected to take weeks for a full return to normal navigation. Iran warned on June 26 that passage through the Strait of Hormuz is "only permitted" via routes designated by Tehran. The Islamic Revolutionary Guard Corps (IRGC) has informed mediators that if it cannot obtain guarantees of Iran's sole control over the Strait of Hormuz in Doha talks, it will close the waterway again. Iran also emphasized that the clause in the MoU regarding free passage through the strait is "only valid for 60 days," and Iran "will under no circumstances relinquish its rights in the Strait of Hormuz." U.S. Vice President Vance clearly stated that he is "absolutely confident the Strait of Hormuz will remain open for free navigation, and at no additional cost." The divergence in positions on this issue has not been bridged, and the institutional arrangements for strait transit remain uncertain.

Second-layer logic: Supply-side structure is tight. Data from the American Petroleum Institute (API) showed that U.S. crude inventories fell by 6.072 million barrels for the week ending June 26, exceeding the market expectation of a 4.05 million barrel decline. The continuation of the destocking trend provides a floor for oil prices. The International Energy Agency (IEA) has previously warned that the global oil market could enter a "red zone" in July-August 2026, facing severe supply shortage risks. The IEA forecast a global oil supply gap of 1.78 million barrels per day in 2026.

Third-layer logic: Shift in analyst expectations. A Reuters survey released on July 1 showed that analysts have lowered their 2026 oil price forecasts for the first time since the Iran war began, ending a five-month streak of upward revisions. This downgrade is set against the backdrop of the reopening of the Strait of Hormuz alleviating market concerns about long-term supply disruptions. However, the news of Iran's refusal for direct meetings means this "alleviation" may be fragile and reversible.

In summary, oil prices are shifting from "cyclically driven" to "event-driven with structural risk resonance." Brent crude fell by about $45 per barrel in the second quarter, the largest quarterly drop since the 2008 financial crisis. This huge decline itself means the market had priced in a considerable degree of geopolitical risk resolution in Q2. After Iran refused the meeting on July 1, the rebound in oil prices, though limited in magnitude, sends a clear directional signal — the risk premium is being repriced, and this process may run through the entire third quarter. Analysts at Mitsubishi UFJ Financial Group (MUFG) said: "The improving prospects for a lasting U.S.-Iran agreement continue to ease supply concerns." However, "uncertainty remains over key issues including Iran's nuclear program and the future jurisdiction of the Strait of Hormuz, which could complicate negotiations during a ceasefire."

Crypto Market: Macro Transmission and Capital Structure Changes

The transmission of rising oil prices to crypto assets is not linear, but unfolds through macro liquidity channels.

The transmission chain is as follows: Rising oil prices push up inflation expectations → Expectations for the Federal Reserve to maintain high interest rates are extended → U.S. dollar liquidity tightens → Risk asset valuations come under pressure. At the same time, geopolitical uncertainty itself triggers safe-haven demand, and under this framework, Bitcoin exhibits a dual attribute of being both a "macro hedge asset" and a "liquidity-sensitive asset" — two forces that often pull in opposite directions.

Bitcoin: Pressure under Dual Attribute Structure. As of July 1, 2026, Bitcoin (BTC) was at $58,706.1, down 1.17% over 24 hours, 7.63% over 7 days, and 10.73% over 30 days. During Asian trading, Bitcoin briefly fell 1.5% to $57,742, hitting its lowest level since September 17, 2024. Bitcoin has fallen more than 50% from its all-time high of over $126,000 in October 2025. In the second quarter, Bitcoin dropped close to double-digit percentage points, while the S&P 500 rose about 14% and the Nasdaq 100 rose about 25% over the same period. This stock-crypto divergence indicates that crypto assets are currently more influenced by their own liquidity/positioning dynamics and cross-asset macro pressures, rather than simply following equity beta.

The decline in Bitcoin is jointly driven by macroeconomic uncertainty and broader risk aversion, not by a deterioration in the asset's fundamentals. Citigroup on July 1 lowered its price forecasts for Bitcoin and Ethereum, citing persistent ETF outflows as a major factor. Citigroup's bear case lowered the one-year target price for Bitcoin to $53,000 and for Ethereum to $1,094. Market expectations of "higher for longer" U.S. interest rates, a strong dollar, and the continued capital absorption effect of sectors like AI collectively lead institutions to reduce exposure to risk assets.

In the options market, put options have accumulated considerable open interest in the $58,000–$55,000 range, potentially forming a price "attractor" before expiry. Demand for downside protection increased, especially for Bitcoin put options expiring in July with strike prices of $55,000–$58,000.

Ethereum and Altcoins: Beta Amplification Effect. Ethereum (ETH) was at $1,574.94, down 0.84% over 24 hours, 7.38% over 7 days, and 20.92% over 30 days, with a significantly larger retracement from its yearly high than Bitcoin. Ethereum has fallen to its lowest level since September 2024. Altcoins, as high-beta assets, typically face larger drawdowns during geopolitical-driven macro uncertainty.

Stablecoins: On-Chain Mapping of Safe-Haven Demand. On-chain data shows that stablecoin inflows to centralized exchanges (CEXs) are accelerating. According to on-chain analyst monitoring, as of July 1, approximately $770 million of stablecoins (USDC and USDT) raised by Pump.fun through public offerings had flowed into CEXs. Santiment data also shows that over the past 24 hours, large addresses have transferred significant amounts of ETH, stETH, as well as stablecoins like Ripple USD, Ethena USDe, and Global Dollar USDG to CEXs.

Stablecoin inflows to exchanges are usually interpreted as a sign of funds preparing to build positions. However, given the current coexistence of geopolitical uncertainty and macro pressures, this phenomenon may reflect two motivations simultaneously: some funds seek entry opportunities amid volatility, while others use stablecoins for safe-haven allocation. Regardless of interpretation, stablecoin inflows themselves are an objective indicator of market activity and capital attention.

Structural Signals from the Derivatives Market. Option skew remains negative, indicating that market pricing for downside risk is dominant. Implied volatility is at elevated levels, corresponding to higher near-end downside risk premium. This indicates that the market does not view this round of geopolitical shock as a one-time event, but is continuously monitoring potential systemic risks. Some analysts believe that the "pricing regime shift" triggered by geopolitics has not yet been fully digested in the spot market, and the current negative skew is not only an expression of sentiment but also a warning of future liquidity risk.

Macro Transmission and Crypto Asset Linkage Logic Diagram

Market Structure Conclusion: Entering a Geopolitics-Driven High-Pressure Macro Cycle

Synthesizing the above analysis, a structural market judgment can be drawn:

Global asset pricing is entering a "geopolitics-driven macro regime."

This judgment is based on three mutually reinforcing facts:

First, geopolitical risk is shifting from "event-type" to "state-type." The U.S.-Iran diplomatic process has slipped from a dialogue mechanism to a conditional confrontation mechanism, which is not a one-time event but a continuous state. Iran makes the start of final negotiations contingent on the implementation of specific MoU terms; Israel refuses to withdraw from the "security zone" in southern Lebanon; Iran warns it will "respond without hesitation" if the ceasefire agreement is violated. These factors together constitute a geopolitical environment with low negotiation elasticity, the duration of which may far exceed initial market expectations.

Second, the risk premium repricing in the energy market is persistent. The IEA warns of a historically significant supply shortage in Q3; U.S. crude inventories continue to decline; the threat level in the Strait of Hormuz remains "substantial"; approximately 80 mines remain in the main channel. These supply-side constraints mean that the geopolitical risk premium on crude oil will not quickly dissipate due to a single diplomatic statement, but will persist throughout the third quarter.

Third, the crypto market is adapting to a new pricing environment. Demand for put options is strong; large-scale stablecoin inflows to exchanges; Bitcoin has fallen to a 21-month low. These signals collectively point to the fact that market participants are pricing persistent uncertainty, not a one-off shock.

For crypto market participants, this means that traditional "buy and hold" or "simply track macro data" strategies may need reassessment. In a geopolitics-driven high-pressure cycle, risk management tools and hedging strategies will become more prominent, and the allocation value of stablecoins and the protective function of option strategies will become more critical. Against the backdrop of the global market moving from "negotiable geopolitical conflicts" to a "structural stalemate cycle," risk no longer depends on event escalation, but on the continuous evolution of "diplomatic failure itself."

Summary

Iran's refusal of a direct meeting in Doha appears on the surface to be a diplomatic schedule adjustment, but in reality it marks the U.S.-Iran relationship slipping from a "dialogue mechanism" to a "conditional confrontation mechanism" — a new geopolitical cycle with low negotiation elasticity is forming. After experiencing a historic drop of $45 per barrel in Q2, Brent crude stood back above $73 on July 1. The approximately 80 mines remaining in the Strait of Hormuz, Iran's tough stance on control of the strait, and the fundamental disagreements between the U.S. and Iran on nuclear issues and asset unfreezing collectively form the structural basis for the repricing of the risk premium.

Meanwhile, the crypto market is under dual pressure from macro liquidity: rising oil prices strengthen inflation expectations and high interest rate expectations, while tightening U.S. dollar liquidity suppresses risk asset valuations. Bitcoin has fallen to a 21-month low, Ethereum is down over 20% in 30 days, and the accelerated inflow of stablecoins into CEXs reflects the complex sentiment of market capital between seeking safety and waiting for opportunities.

Global asset pricing is entering a high-pressure cycle driven by geopolitics. In this cycle, diplomatic failure itself has become the most central source of risk, and its duration and evolutionary path will profoundly influence the pricing logic for crude oil and crypto assets in the second half of the year.

FAQ

1. How long will the impact of Iran's refusal of the Doha meeting on crude oil prices last?

The duration depends on how long the U.S.-Iran diplomatic stalemate continues. The current deadlock revolves around "conditions fulfillment" (asset unfreezing and regional security issues), while the IEA warns of a potential supply gap of 1.78 million barrels per day in Q3. As long as the institutional arrangements for the Strait of Hormuz are not finalized — including Iran's claim to control, U.S. opposition to tolls, and the demining progress for the approximately 80 mines — the risk premium will be difficult to fully dissipate. Until a new understanding is reached between Washington and Tehran, the market will remain on hold.

2. Why is Bitcoin both seen as a safe-haven asset and under pressure during geopolitical tensions?

Bitcoin has dual attributes as a "macro hedge asset" and a "liquidity-sensitive asset." When geopolitical risks rise, some funds treat Bitcoin as digital gold for safe-haven; but rising oil prices push up inflation expectations, strengthening expectations that the Fed will maintain high interest rates, leading to tight dollar liquidity and pressure on all risk assets. These two forces act simultaneously, creating a tug-of-war for Bitcoin's price. Citigroup on July 1 lowered its one-year target price for Bitcoin to $53,000, reflecting ongoing macro pressures.

3. Are stablecoin inflows to exchanges a bullish or bearish signal?

Stablecoin inflows to exchanges are usually interpreted as a sign of funds preparing to build positions. However, given the current coexistence of geopolitical uncertainty and macro pressures, this phenomenon may reflect two motivations simultaneously: some funds seek entry opportunities at low prices, while others use stablecoins for safe-haven allocation. Data on July 1 showed that Pump.fun alone saw about $770 million in stablecoins flowing into CEXs. Both interpretations have some validity, and the key is whether they translate into actual buying behavior.

4. What is a "geopolitics-driven high-pressure macro cycle"?

It refers to a structural phase where global asset pricing is primarily driven by geopolitical events and where uncertainty remains persistently high. Core characteristics include: diplomacy shifting from a "dialogue mechanism" to a "conditional confrontation mechanism"; energy market risk premiums persisting; and the crypto market facing dual pressures from macro liquidity and geopolitical uncertainty. In this cycle, the importance of risk management tools and hedging strategies will be more prominent.

5. What indicators should crypto investors focus on in the current environment?

It is recommended to focus on three levels: Macro level, monitor oil price trends and U.S. crude inventory changes (API data shows inventories fell by 6.072 million barrels for the week ending June 26); Crypto market level, watch option skew, put option open interest, and ETF fund flows (Citigroup notes persistent ETF outflows as a major pressure source); Capital level, track stablecoin exchange inflow volumes — data on July 1 shows large addresses are accelerating transfers of various stablecoins to CEXs. These three types of indicators together form a monitoring framework for the transmission of geopolitical risk to the crypto market.